Beyond the Next Bill

State of Us: What a windfall reveals about financial pressure and priorities

In Murmuration’s recent partnership with Voto Latino, we asked Americans a simple open-ended question: “What would you do if you woke up tomorrow with an extra $10,000?” And then we asked it again at a different scale: what about $100,000?

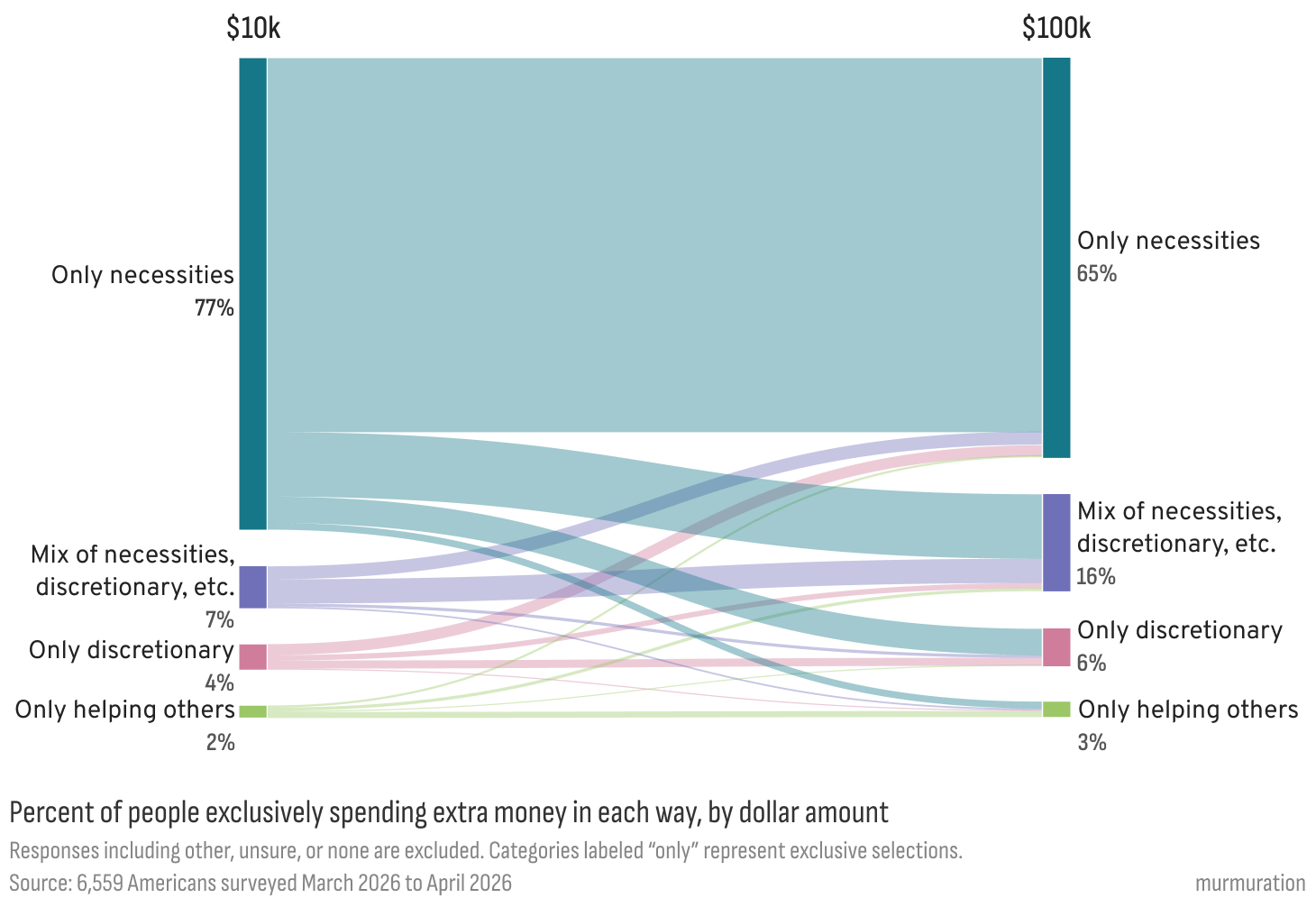

It’s a useful way to understand not just what people need or want, but what they feel they’re missing. Across more than 6,500 respondents, the answers at $10K were almost uniformly categorized as “necessities”—responses like “Pay off loans,” “get my teeth fixed,” or “A car and groceries.” What’s surprising is that even at $100K, the dominant responses remain practical rather than extravagant. People start to think a bit bigger, but the first instinct is still stability, security, and catching up on basic needs.

In the above chart, we display the single best label for each person’s open-ended response. Respondents who mentioned multiple uses for the money (for example, paying bills while also taking a vacation or helping family) were grouped into the mixed category.

A Stable Foundation

But people’s answers were often much richer (no pun intended) than a single category could capture. Many respondents described layered priorities in the same necessities response: paying bills or loans, repairing a car, or putting a little money into savings.

So while the previous chart shows the single best label for each response, the next analysis allows for multi-label classification, capturing all of the themes embedded in what people shared. When viewed this way, a striking pattern emerges: across gender, race, party, education, and income, between 85–89% of Americans said they would spend at least some portion of a hypothetical financial windfall on a core life necessity.

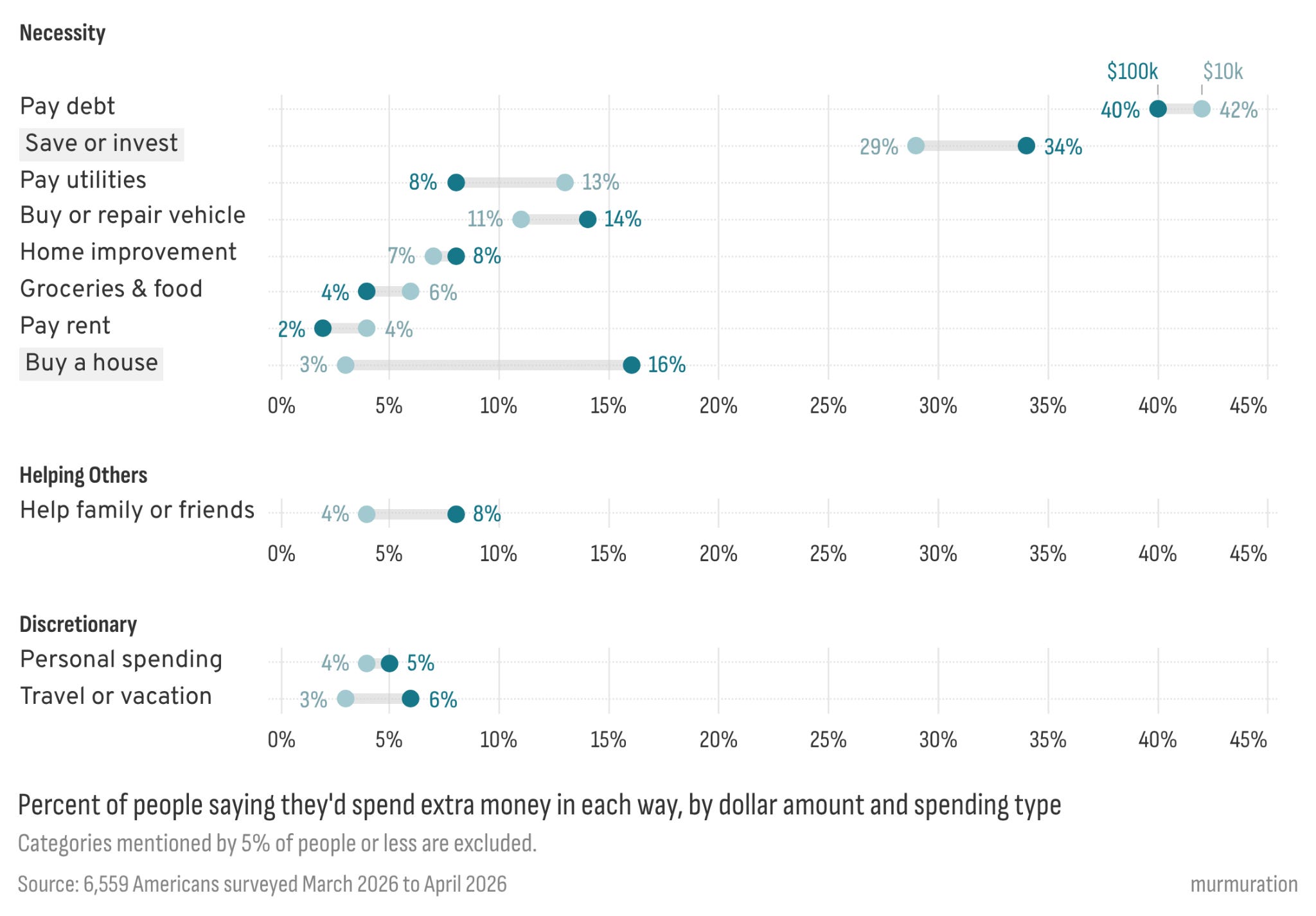

The largest share pointed to paying down debt: credit cards, student loans, mortgages (42% at $10K; 40% at $100K). Others focused on paying utility bills (13% at $10K; 8% at $100K). A third group mentioned maintenance and upkeep: fixing or replacing a broken vehicle (11% at $10K; 14% at $100K), or repairing something in the home (7% at $10K; 8% at $100K).

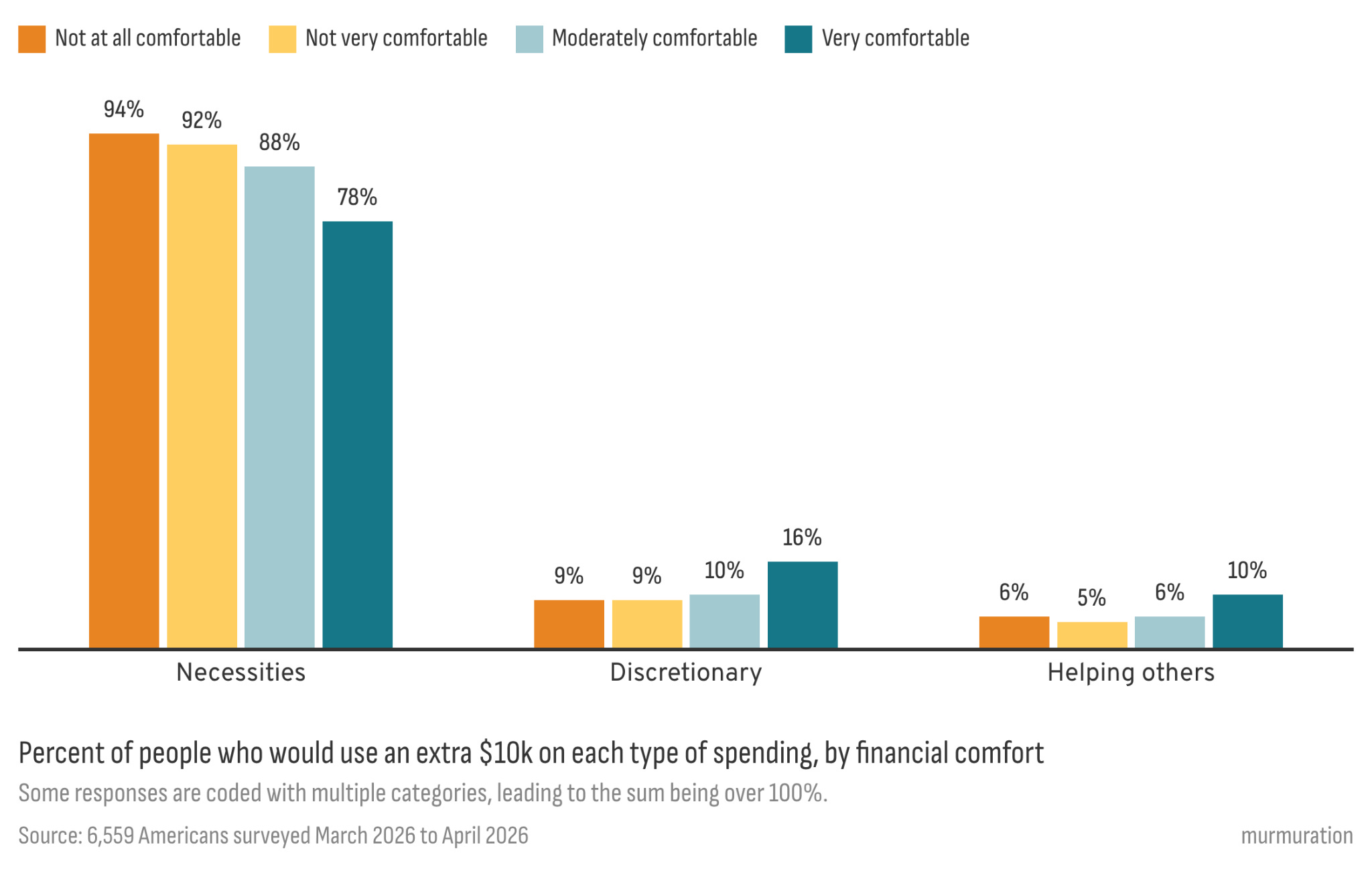

This is not aspirational—it’s stabilizing. Even the differences between Americans at different levels of financial security are narrower than might be expected. With $10,000, those who are not at all financially comfortable overwhelmingly mention necessities (94%, compared to 9% discretionary). But even among the most comfortable, 78% still prioritize necessities, compared to 16% who would use the money for something discretionary. The pattern is the same at $100,000: the share using the money for necessities goes from 90% among the least comfortable Americans to 77% among the most comfortable.

If necessity versus discretion is one axis, there’s another that matters just as much: time horizon. Some necessities are about right now: a bill that’s overdue, a car that won’t start, a roof that’s leaking. Others stretch years or decades into the future: retirement savings, college tuition, home ownership.

At $10,000, a majority of the least financially comfortable Americans (59%) focus on immediate needs, compared to just 16% of the most comfortable. In contrast, the prevalence of long-term thinking increases from just 5% among the least comfortable to 24% among the most comfortable. The same pattern appears at $100,000. The focus on immediate needs declines from 40% to 10% at the highest comfort level, while long-horizon thinking expands from 14% to 36%.

Building Toward the Future

The single largest shift in Americans’ thinking when imagining the jump from a $10,000 to a $100,000 windfall is the desire for owning a home. At $10,000, just 3% of Americans say they would use the money to help buy a home. At $100,000, that number rises to 16%—more than a fivefold increase. The increase in home-buying responses is greatest among those with the least financial comfort: from 6% at $10,000 to 23% at $100,000. Among those who are already comfortable, mentions of homeownership rise from 3% to 10%. The further someone is from homeownership today, the more powerfully they reach for it when it feels even remotely attainable.

But homeownership is only part of a broader pattern. When Americans imagine having some financial breathing room, they are most often describing investment: in stability, in opportunity, and in the future they want to build. Many mention putting money into savings vehicles like CDs, retirement accounts, or high-yield savings. Others take a more active approach: more than a hundred respondents explicitly say they would start a business.

That same instinct extends outward. Giving increases as the windfall grows: 6% of respondents mention donating or helping others at $10,000, rising to 10% at $100,000. The recipients are often close to home—churches, children, parents, neighbors. But many also point to broader needs: dozens explicitly mention helping people experiencing homelessness. Some responses are deeply personal. One person describes housing a homeless brother. Two others talk about helping house their own children.

An extra $100,000 doesn’t guarantee a home, a business, or long-term security. But for many, it at least makes those things imaginable and once that hypothetical door opens, people move from patching what’s broken to imagining what could be built.

Final Thoughts

We asked this question to understand what people might want with fewer constraints. What we heard back wasn’t extravagance. It was steadiness. Yes, people want vacations. Yes, they want to treat themselves. But that isn’t the center of the dream. The dream is closer to home: opportunity, growth, and a sense of safety and security.

And that raises a different set of questions, not about what people want, but about what makes that possible:

Why does something as fundamental as homeownership still sit just out of reach for so many and what would it take to change that?

How much untapped potential—entrepreneurial, civic, relational—is sitting dormant simply because people don’t have the margin to act on it?

And what would our communities look like if more people had not just enough to get by, but enough to look ahead?

Because for most Americans, the dream isn’t more. It’s finally having enough to exist comfortably or move forward with more confidence.

Just stable enough to build from.

Murmuration is a non-profit that organizes a network of partners and equips them with the insights, tools, and services needed to help communities build and activate the power to transform America into a nation where everyone thrives. murmuration.org