The conversation about the cost of living in America has been going on for years. It surfaces every election cycle, often as the top issue, and yet very little about the underlying experience seems to change. The prices of groceries, gas, and housing continue to climb, and for many people, the gap between what they earn and what it costs to live keeps widening.

This month, Murmuration partnered with Voto Latino to field a national survey of 6,559 Americans focused on the experience of living inside this economy. We asked how people are managing, what they’re cutting back on, and how they’re thinking about their financial futures.

We started with a simple question: what is the biggest problem in your life right now?

For almost half (48%) of Americans, the answer is money. But that burden isn’t evenly distributed. It’s even higher among young adults (55%), those in their prime working years (53%), women (53%), and Hispanic or Latino respondents (52%).

The Cost of Daily Life

To understand how that pressure shows up in people’s lives, it helps to start with the basics.

When we asked people to describe their current level of financial comfort, a majority—56%—said they are not comfortable. That includes people who are struggling to cover basic expenses, as well as those who can technically pay their bills but feel like money is always tight. Only 11% describe themselves as very comfortable, with no major financial concerns. In other words, most Americans are living right on the edge.

For many, an unexpected expense of even $500 would pose a serious challenge. More than half of Americans (52%) have no immediate way to pay. Some would take on credit card debt (16%), borrow from family or friends (10%), or need to sell possessions to raise funds (8%). Fully 18% of Americans say their household would not be able to cover a $500 emergency at all.

Why is money so tight? Over the past year, 50% of Americans point to the cost of food and groceries as one of the top three expenses putting strain on their household budget. Utilities follow at 40%, then rent or mortgage at 37%, and gas or transportation at 32%. These aren’t frivolous, discretionary expenses. They are the necessities and fixed costs of everyday life.

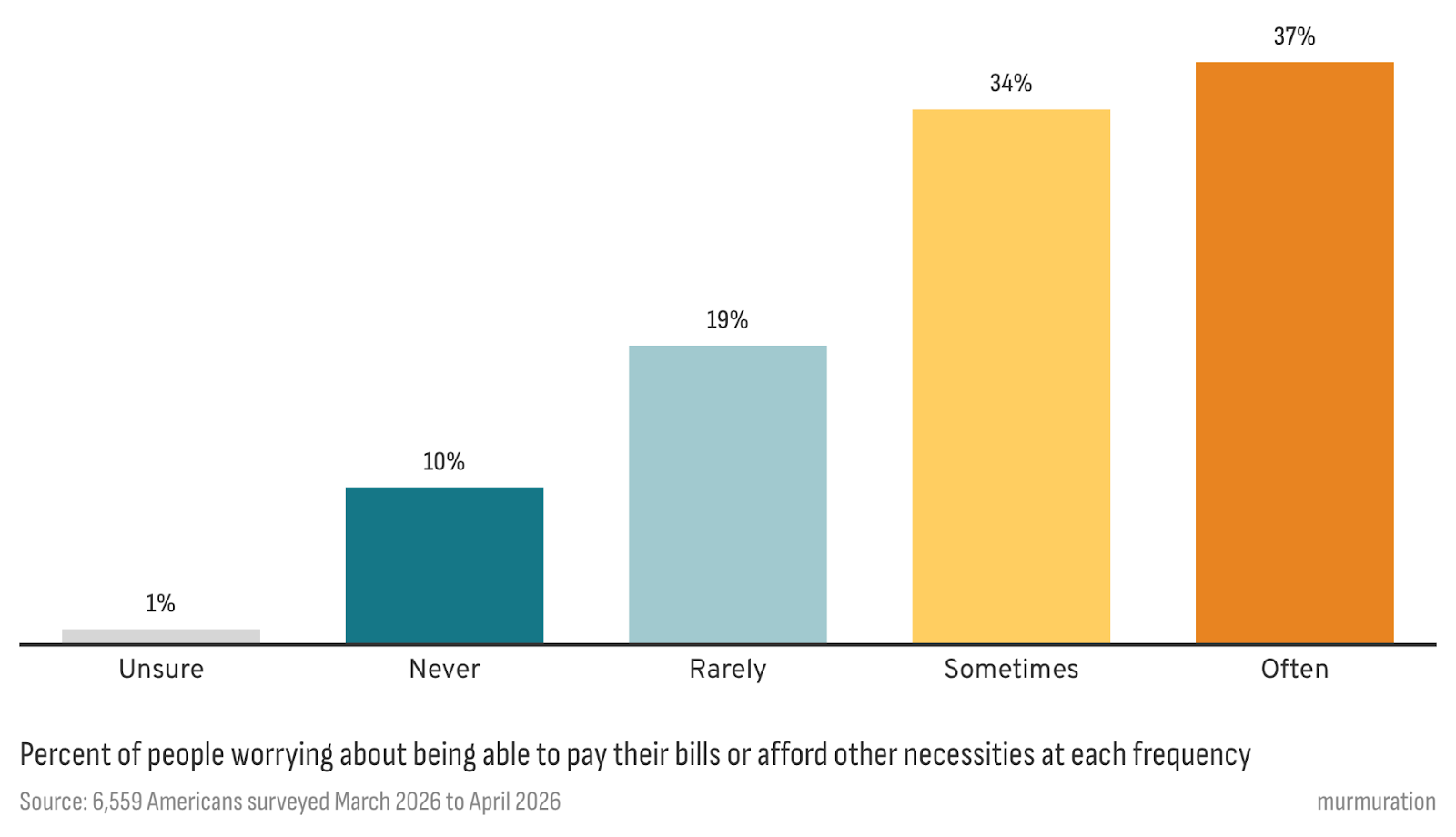

Overall, 62% of Americans say it has become harder to afford everyday expenses compared to just a few years ago (32% much harder, 30% somewhat harder). And for many, the distress caused by rising costs isn’t occasional—it’s constant. Roughly 7 in 10 Americans experience financial worry on a regular basis.

From Adjustment to Triage

When expenses go up, people adjust. They make tradeoffs. What emerges from these choices is not just a set of isolated behaviors, but a hierarchy of sacrifice.

The response to rising gas prices, in particular, offers a window into how people’s lives have been forced to change. Almost half of Americans (48%) say they’ve cut back on driving or travel because of gas prices. But the impact doesn’t stop at fewer trips: 34% say they are spending less on other essentials to make up for what they are paying for gas, and 15% have changed their work or commute habits entirely.

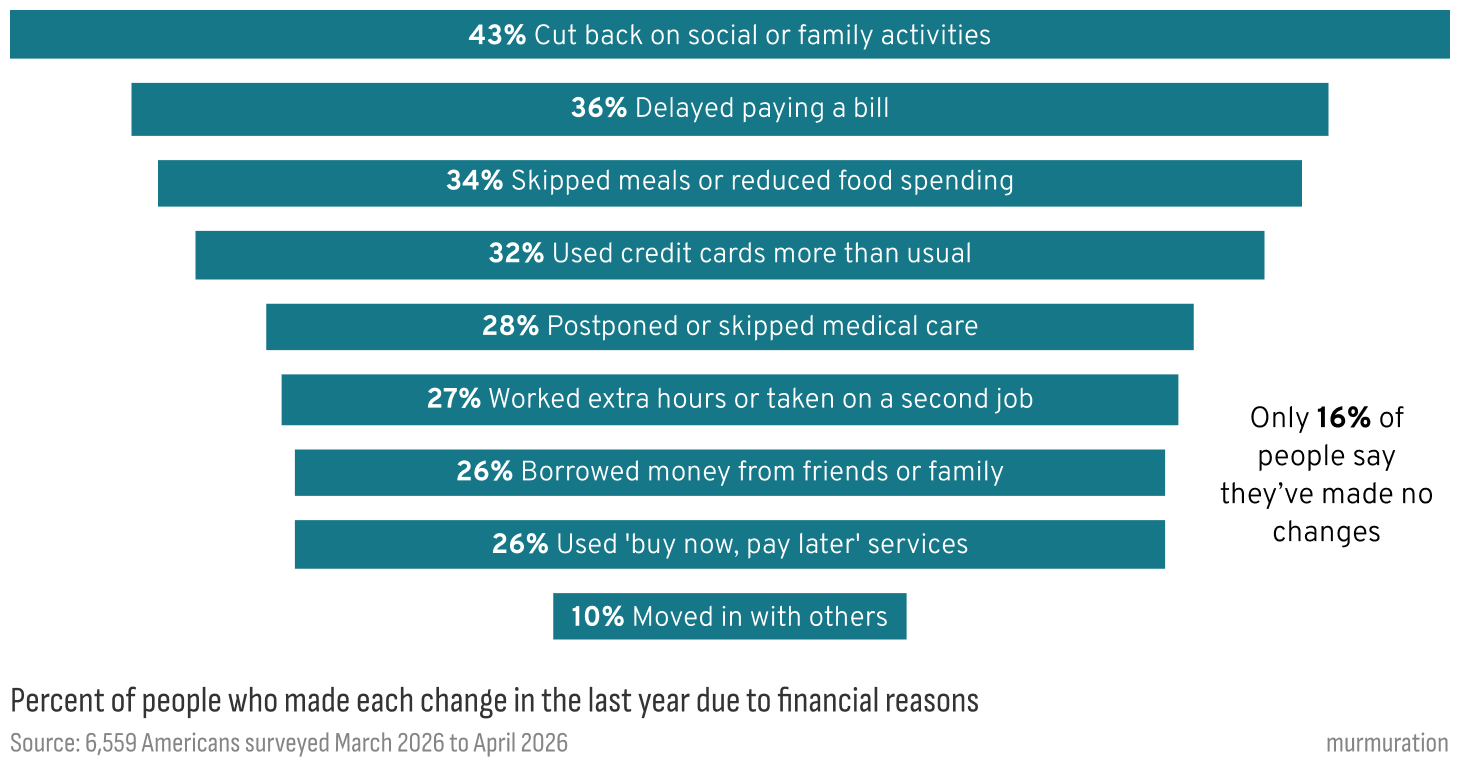

More broadly, people are making significant, life-altering decisions for financial reasons alone. Things that should be high priorities, that characterize our basic quality of life and ability to live stress- and worry-free, are falling by the wayside. Things like cutting time with friends and family, delaying paying bills, postponing medical care, or even skipping meals and reducing food spending.

The data suggests that people start by cutting what feels optional: dinners out, gatherings, small moments of leisure. But as pressure builds, those tradeoffs move inward. Food budgets shrink. Medical care gets delayed. Bills are pushed. What begins as adjustment becomes constraint, and then something closer to triage. These are not one-time decisions. They are ongoing calculations about what can be postponed, reduced, or given up entirely.

Same Problem, Different Blame

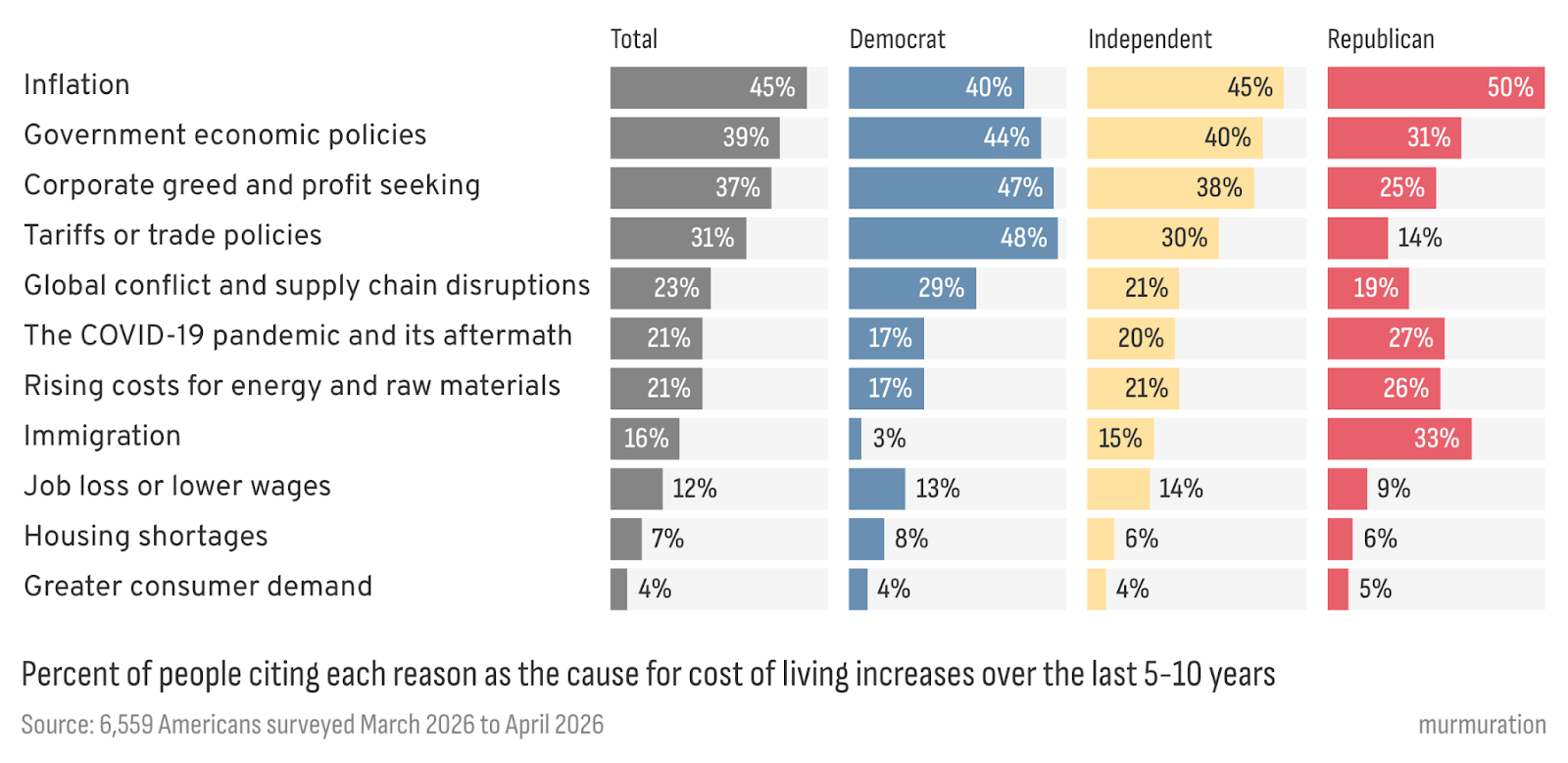

Americans hold multiple, overlapping theories for why the cost of living has become more expensive over the past five to ten years. They assign responsibility broadly across both the private sector and government. But Democrats and Republicans tell very different narratives about what (and who) is to blame:

While Democrats see corporate greed and trade policy as having the biggest impact, Republicans are more likely to blame the COVID-19 pandemic, energy costs, and the effects of immigration for the rising cost of living.

One thing that people do broadly agree on is that the president, Congress, and other elected officials can impact families’ ability to afford everyday expenses. Nearly two-thirds (62%) say that political leaders have a lot of influence on the economy; another 26% say they have at least some influence. Only 9% believe that elected officials have little to no power over basic affordability.

Yet there is a noticeable lack of optimism about where things are headed. Only 36% of Americans believe their financial situation will improve over the next few years. More than one in five (21%) expect things to get worse, and 38% say they’re simply unsure. For many, the future feels less like a trajectory and more like a question mark.

That same sense of strain extends to the bigger milestones that have long defined the American dream. When we asked whether buying a home, raising a family, and retiring comfortably felt realistic, 31% said these goals are mostly out of reach. Another 34% said they’re possible, but difficult to achieve. Just 25% said these goals feel fully within reach.

Relief, Not Reinvention

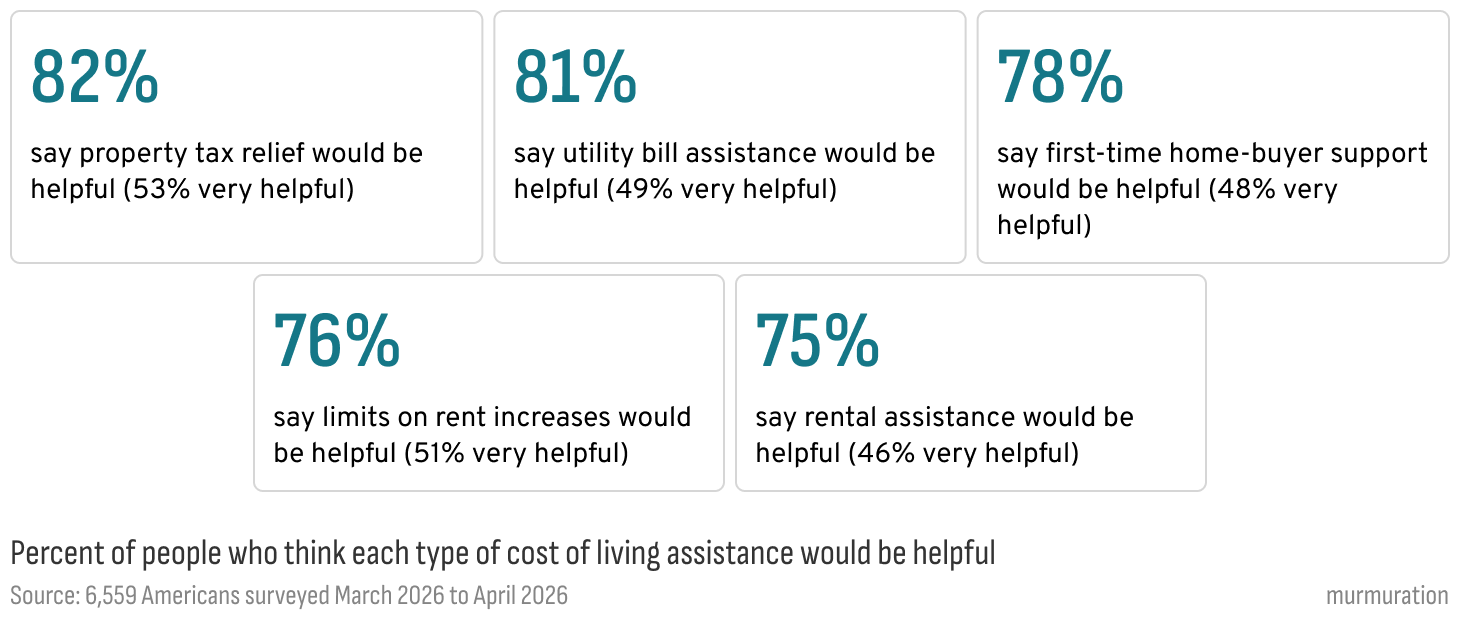

There’s actually a surprising amount of agreement on steps that Americans believe would make things better. There is strong support for policies that directly reduce or stabilize the core costs of living—particularly housing and utilities:

Housing, in particular, stands out as the area of strongest agreement—not just overall, but across political lines. Property tax relief is rated as “very helpful” by 62% of Trump voters and 48% of Harris voters. Limits on rent increases are seen as helpful by 59% of Trump voters and 90% of Harris voters. First-time homebuyer support is viewed as helpful by 72% of Trump voters and 85% of Harris voters. In a landscape where consensus is often hard to find, housing affordability emerges as one of the clearest areas of overlap.

There is also meaningful support for policies that address income and debt more directly. About 68% say increasing the minimum wage would be helpful, and 64% say the same about student debt relief. These solutions operate on the other side of the equation—either increasing what people earn or reducing what they owe—but they point to the same underlying imbalance.

Final Thoughts

The story this data tells is not just about money. It’s about the conditions under which people are living their lives and how those conditions are forcing people to change in response to accumulating economic pressure.

For decades, there has been an implicit promise at the center of American life: that if you work hard, you can get ahead. But for many, that promise no longer feels true. Today, 69% of Americans say that even “people who work hard struggle to get ahead financially”.

At the same time, people are not confused about what would actually make a difference. When asked what would help most, 28% point to lowering the cost of everyday essentials like food, gas, and utilities, while 18% say wages that keep up with the cost of living would matter most, followed by housing costs and taxes (11%), healthcare (9%), and debt (9%). They are a set of clear, immediate pressures that shape daily decision-making.

And those decisions are increasingly defined by tradeoffs. When nearly half the country is cutting back on time with family and friends, even connection itself starts to become a luxury. The slow erosion of gathering, celebration, and everyday togetherness doesn’t show up in economic indicators, but it reshapes how people experience their lives, their communities, and their sense of belonging.

These are some of the questions that follow:

How should institutions respond to a population where financial insecurity is the norm rather than the exception?

What happens to a society when people can no longer afford to show up for each other, not just economically, but socially and emotionally?

How does a life organized around constant tradeoffs change what people expect from the future?

What this data makes clear is that the financial strain Americans are living with is a structural reality, built up over years and felt in grocery aisles, doctor’s offices, and kitchen tables across every region of the country.

Hard choices, not inevitable ones.

Murmuration is a non-profit that organizes a network of partners and equips them with the insights, tools, and services needed to help communities build and activate the power to transform America into a nation where everyone thrives. murmuration.org

Voto Latino is a civic advocacy organization dedicated to educating and empowering the next generation of Latino voters while working to build a more inclusive and representative democracy. votolatino.org